Starting a business is a rush, but the "funding wall" is real. You’ve got the vision, you’ve got the grit, but then you look at your bank account or your personal credit score and realize that traditional banks aren't exactly rolling out the red carpet for you.

If you’ve ever walked into a local bank looking for a working capital loan only to be told you need five years of tax returns and a perfect 800 credit score, you aren’t alone. Traditional lenders make it hard because they’re stuck in an old-school mindset. They see a "new owner" and see "risk."

But here’s the truth: your business’s potential isn't just a number on a FICO report. You can get the startup funding you need without trashing your personal credit in the process. At Loan Pros, we specialize in being the matchmaker for businesses that are ready to grow but need a partner who understands the modern landscape.

Before we dive into the steps, let’s get the "Universal Floor" out of the way. To work with our network of 75+ lenders, you generally need to meet these four benchmarks:

- At least $10,000 in monthly gross revenue.

- At least 3 months of business bank statements.

- A dedicated business bank account (we cannot fund personal accounts).

- A U.S.-based business.

If you hit those marks, you aren't just "applying", you’re effectively overqualified for some of the best programs on the market. Here is how you navigate the funding world while keeping your credit safe.

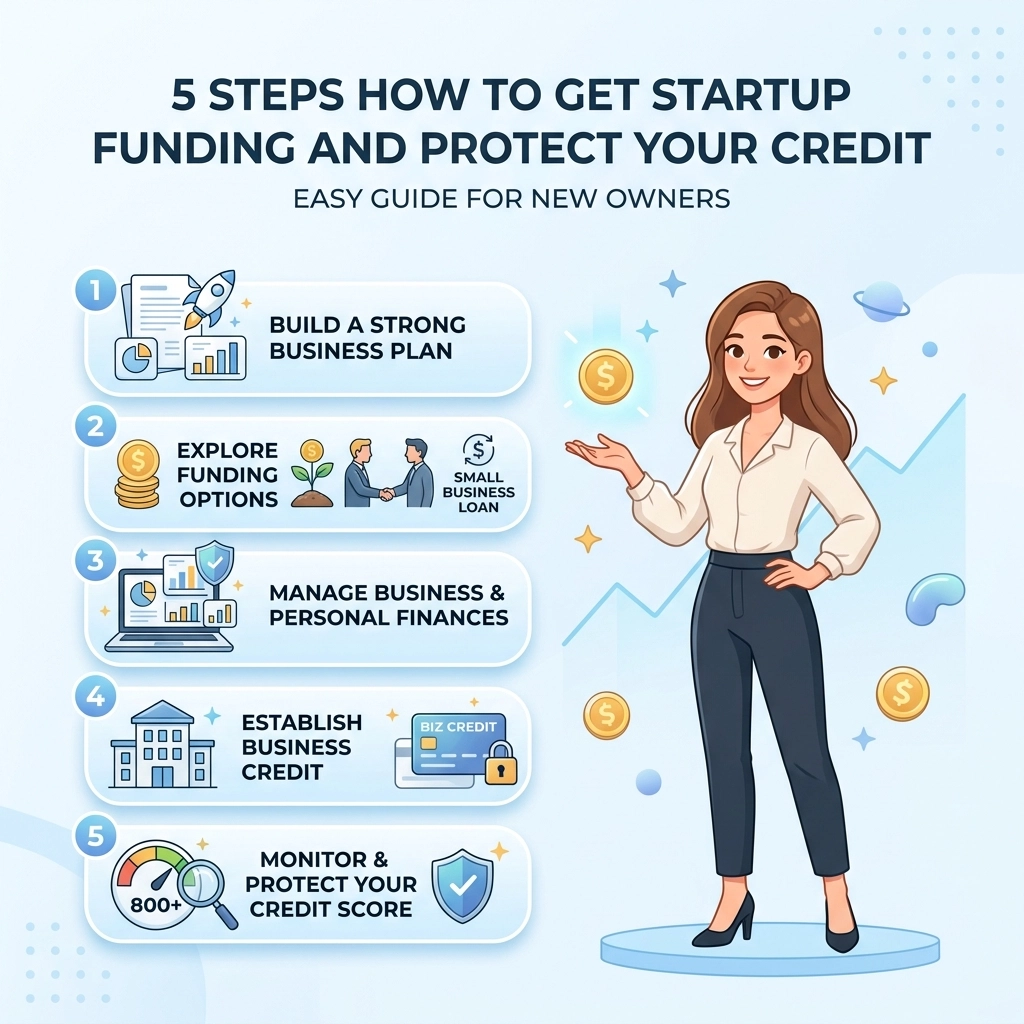

Step 1: Establish Your Business Entity Correctly

You might be tempted to run everything as a sole proprietorship to keep things simple. Don't do it.

If you want to protect your personal credit, you need to draw a line in the sand between "You" the human and "You" the business. This starts with registering your business as an LLC or a Corporation.

When you operate as a sole prop, your personal Social Security Number is the only thing lenders can look at. When you establish a formal entity and get an Employer Identification Number (EIN) from the IRS, you begin building a separate credit profile for the business itself.

Think of it as giving your business its own identity. This is the first step in ensuring that if the business needs a small business funding boost, it’s the business’s reputation on the line, not your personal ability to buy a house or a car later. Check out our Smart Biz Funding Guide for more on setting up for success.

Step 2: Separate Your Personal and Business Finances

This is where many new owners trip up. You’re using your personal debit card for a quick office supply run, or you're depositing client checks into your personal savings.

Stop right there.

Lenders, especially the high-quality ones in our network, want to see clean, professional records. We require at least 3 months of business bank statements. If those statements are a messy mix of grocery trips and business expenses, it’s a red flag.

By opening a dedicated business bank account, you accomplish two things:

- Credibility: You look like a professional operation, not a hobby.

- Credit Protection: It prevents "commingling," which can lead to personal liability if the business ever faces legal trouble.

Remember, at Loan Pros, we do not accept personal accounts for funding. Having that business account ready is your ticket to Funding Options that aren't available to the average person on the street.

Step 3: Understand Performance-Based Lending vs. Credit-Based Lending

Most people think "business loan" equals "credit score check." Not true.

There is a massive world of performance-based lending. This is where lenders care more about your revenue and cash flow than your FICO score. If your business is consistently doing $10k, $25k, or $50k a month in gross revenue, that is a much stronger indicator of your ability to repay than a late credit card payment from three years ago.

This is why we offer programs with no minimum FICO requirements. We look at the health of your business. Are you growing? Do you have consistent deposits? If the answer is yes, you can often secure a working capital loan based on your performance.

This is a game-changer for owners who might have "bruised" credit but a booming business. If you're worried about your score, read our guide on business funding with bad credit. You'll see that you're not stuck.

Step 4: Use a Soft-Pull Application to Explore Options

One of the biggest mistakes new owners make is "rate shopping" by submitting full applications to five different banks. Each one of those banks does a "hard pull" on your credit.

A hard pull can drop your score by several points. Do that five times in a month, and you’ve just done real damage to your credit before you’ve even seen a dime of funding.

At Loan Pros, we do things differently. Our online application takes about 15 seconds and uses a NO hard credit pull process to see what options you qualify for. We believe you should be able to explore your How it Works page and see your potential funding without any "penalty" on your credit report.

Insider Secret: Lenders love to see that you are protective of your credit. By using soft-pull tools, you’re acting like a seasoned CFO, not a desperate borrower.

Step 5: Leverage a Network of Lenders to Find the Right Fit

Why go to one bank and hope they say yes when you can go to 75+ lenders simultaneously?

When you work with a capital matchmaker like us, you aren't just applying for one product. You are entering a network where lenders compete for your business. This is where the "Overqualified = Qualified" mindset kicks in. If you have the revenue and the bank statements, you are a hot commodity in our network.

This approach saves you time and: more importantly: protects your credit from multiple inquiries. Instead of a dozen different applications, you do one. Then, you get a funding decision in as little as 24-48 hours.

Why Speed and Strategy Matter

In the freight world or any fast-moving industry, an opportunity doesn't wait for a 60-day bank approval process. If you need to fix a truck, buy inventory, or bridge a gap in your cash flow, you need that capital now.

By following these five steps, you aren't just getting a loan; you’re building a financial foundation. You’re keeping your personal credit pristine while leveraging your business’s actual performance to get the fuel you need to grow.

Ready to see what you qualify for?

It takes 15 seconds, and it won't hurt your score. Check out our FAQ if you have more questions, or jump straight to the application to see your options.

Actionable Next Step:

Gather your last 3 months of business bank statements today. Even if you aren't ready to pull the trigger this afternoon, having those PDFs ready to go means you can move at the speed of business when the right opportunity strikes.

Disclaimer: Loan Pros provides financial matchmaking services. We are not a direct lender. Funding availability, terms, and conditions are subject to individual lender requirements and credit approval. Always consult with a financial advisor before taking on business debt. For more details, see our Terms and Privacy page.

Leave a Reply